A guide to help businesses compare business loans

When you have big plans for your business, getting the funds you need to put them into action is vital for business growth and ultimate success. Whether you need funds to buy stock or equipment, hire extra staff, to do a new fit-out, expand your business, or simply to cover cash flow, there are so many types of loans to choose from.

With all the business finance options available in the market today, conducting a business loan comparison and knowing which type of loan to choose can be a challenge. You don’t want to miss out on opportunities when they pop up, so it helps to know a bit about your options well in advance.

Below you’ll find a handy snapshot of a range of different types of loans to help you compare business loans for yourself. From interest rates to loan terms, from lending criteria to the application process, knowing a bit about each finance option will help you weigh up the pros and cons, and find the right solution for your needs.

An unsecured business loan is a broad-ranging finance option that can be used for any business-related purpose. It differs from a secured business loan in that no security is required to access the funds.

It is a short term funding facility with terms of around one or two years. You get a repayment schedule for the term, with weekly repayments. You don’t need security to access the funds.

Borrow anywhere from $5,000 to $300,000 or more over terms of between 3 and 36 months. Because the loan is riskier, being unsecured, the interest rates are usually higher. A personal guarantor may be required too.

The application process is typically quick and easy, and the process usually happens online. The funds are available in as little as 24 hours which means they are a great option for businesses that can’t wait for the funds. They are also good when the business doesn’t meet the lending requirements of banks and other traditional funders.

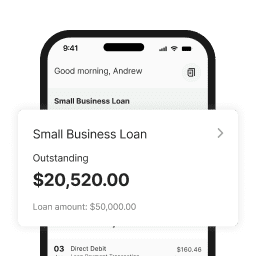

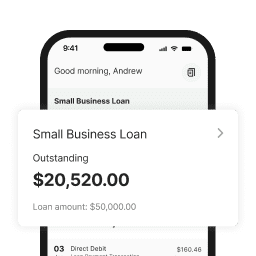

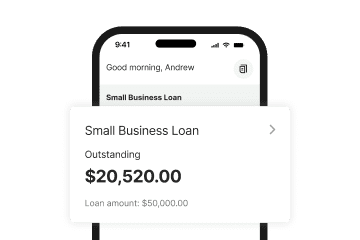

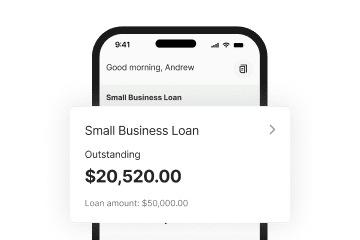

Find out more about the Prospa Small Business Loan

Unsecured business loans are great for:

- Investing in machinery or equipment

- Renovations or fit-outs

- Purchasing stock, tools or equipment

- Business growth or expansion opportunities

- Marketing campaigns or promotions

- Developing a website

- Buying office or café furniture

- Paying tax or BAS lump sums

Line of credit

A line of credit provides ongoing access to an agreed amount. It’s there when you need it and you often only pay interest on funds you use, not the whole amount.

Line of credit products vary widely but limits typically are available up to $100,000, with some providers offering larger limits of up to $250,000. Terms range from 3 to 36 months, depending on the chosen provider.

This extremely flexible form of finance acts as a handy safety net for businesses to ride the ups and downs of the cash flow cycle. There are usually no restrictions as to what business purpose you can use a line of credit for.

The application process is quick and easy in most cases, businesses can then simply use the funds as and when required and repay then redraw them throughout the term. Some line of credit products incur fees even when they aren’t used, so make sure you ask. Plus, you will usually need to reapply for your line of credit at the end of the loan term.

Find out more about the Prospa Line of Credit

A line of credit is great for:

- Managing fluctuations in cash flow

- Paying staff wages

- Covering unpaid invoices

- Buying urgent stock

- Managing seasonal fluctuations

- Paying suppliers

- BAS payments

- Much more

Invoice finance

Invoice finance, also known as factoring, is a handy way businesses can unlock their cash flow.

When an invoice is unpaid, it can affect cash flow. But with invoice finance, there’s no need to wait for your customer to pay you. You invoice the customer, then send a copy of the invoice to the finance provider. They provide the agreed amount upfront (up to 80%), usually in as little as a day.

It is then their responsibility to collect the debt from your customer. Once the invoice is paid by your customer, the invoice finance company will send you the remaining funds (minus their fees). This form of finance reduces the impact of late or non-payment of invoices on your business.

On the down side you don’t get the full amount of the invoice value and the fees may be expensive. It’s also hard to set up if you don’t have an established sales history

Invoice finance is great for:

- Short term finance issues

- Supporting working capital

- Purchasing stock

- Investing in tools or equipment

- Paying tax debt

- Much more

Merchant cash advance

A merchant cash advance is an alternative option for businesses who need a cash lump sum for any worthwhile business purpose.

It’s suitable for businesses who have a high turnover and frequently process credit card and EFTPOS sales – but don’t have great access to cash – such as the retail and hospitality industries.

The way it works is that the lender looks at past merchant account sales and advances the funds based on expected future sales. The business then repays the funds (along with any fees) at an agreed percentage of future daily sales. It’s a quick and easy way to access a cash lump sum.

Merchant cash advances can often be more expensive than other loan types, and they can come with restrictive terms and conditions.

A merchant cash advance is great for:

- Purchasing stock or equipment

- Business expansion

- Covering cash flow shortages

- Increasing staffing levels

- Promotions, marketing or a website

- Any other worthwhile business purpose

Equipment finance

When you need to purchase equipment, vehicles or machinery for your business, equipment financing is a funding option. Usually the equipment is secured against the loan amount, which can help to minimise interest rates.

You can borrow anywhere from $5K up to $2 million, sometimes more. And loan terms range from 1 year to 5 years or more. The process is a little more involved, so you may need to give yourself a week or two to organise an equipment finance loan.

With equipment finance, no deposit is required upfront which helps to minimise the impact on cash flow. On the down side, there may be high fees if you want to get out of the loan contract early. Plus, the asset is effectively “owned” by the lender throughout the term of the contract

- Equipment

- Vehicles

- Machinery

- Plant

Hire purchase

Hire purchase is a way of purchasing an item of plant or machinery by ‘hiring’ it over a fixed term. Unlike equipment finance or a lease arrangement, you will probably need to pay a deposit when you take out a hire purchase agreement.

During the term of hire purchase, you don’t own the asset. It is owned by the lending company until the end of the finance term. Once the loan term is completed, the title will transfer to you. You may have the option of a ‘balloon payment’ to lower the amount of regular instalments. Plus you are free to purchase the item at any time – but there will probably be fees associated with this.

Hire purchase amounts range from $5K up to around $2 million, depending on what business item you are looking for. Terms range from 12 months to 7 years or more.

Hire purchase can be used to acquire:

- Equipment

- Vehicles

- Machinery

- Plant

Commercial bill of exchange

A commercial bill of exchange is a flexible type of business finance which can be used to cover shortfalls in working capital – such as those experienced by seasonally affected businesses – or to make approved business purchases.

Usually, a commercial bill of exchange is a short term facility set over loan terms of between 30 days and 180 days (or more by agreement). Funds can be drawn down as required, similar to a revolving line of credit.

You may find fixed interest rates or variable interest rates, depending on the agreement. And interest can be paid up front or on maturity of the term. The term is usually able to be rolled over at maturity, if the borrower desires.

In most cases the minimum loan amount for a commercial bill of exchange is $500K so this type of business finance is only suitable for established, medium to large sized businesses. While an unsecured commercial bill of exchange is possible, they are usually secured against residential property, business property or other assets.

A commercial bill of exchange can be used for:

- Approved business purchases

- Covering working capital

- Commercial investments

Business overdraft

Working in a similar way to a line of credit, a business overdraft is a safety net attached to a business bank account that allows your business to draw more funds out of the account than are actually there (up to an approved limit).

You don’t pay interest on the overdraft funds you don’t use, however you will be charged an interest rate (usually daily) on the money you use. Business overdraft interest rates are often higher than business loan interest rates.

Business overdrafts are available over a term, which can often be renewed at the end. The overdraft may be unsecured, or secured against a property or other asset. With secured overdrafts often attracting lower interest rates.

There may be other fees including application fees, annual fees and late payment fees – and these will apply whether you use the funds or not.

A business overdraft can be used for:

- Paying staff wages

- Buying stock

- Paying suppliers

- Covering invoice gaps

- Unexpected business expenses

- Much more

Traditional business loan

This type of business loan is most commonly available from banks and other traditional lenders. Similar to a mortgage, it consists of a longer fixed-term borrowing facility. Traditional loans are usually secured business loans, that use assets like your home or other property as security against the funds.

Amounts are available from $50K up to $10 million or more over loan terms ranging from 12 months to 10 years or longer.

Arranging a traditional business loan can be a long and cumbersome process, with many hurdles to overcome, and these loans are usually only available to stable, established businesses.

A traditional business loan can be used for:

- Purchasing buildings

- Competitor buy-outs

- Opening new locations

- Business expansions

- Much more

Personal loans

Some business owners opt to take out a personal loan to make business purchases or to support cash flow.

A personal loan can be relatively easy to get, depending on your personal credit rating. Amounts are on the low side, between $5K and $40K over loan terms of 12 months to 3 years. You can usually pay out the loan early with no penalty.

Personal loans are different from other loans (like secured business loans) because they are usually not secured against the asset, so you can use the funds for anything you like. If you plan to purchase a vehicle with a personal loan, the vehicle may be used as security against the loan.

The downside is that the borrower is personally responsible for the loan repayments, not the business.

A personal loan can be used for:

- Business purchases

- Vehicles

- Equipment

- Machinery

Business credit card

A business credit card is a convenient, flexible finance option for businesses. They are great for short term cash flow support with credit limits ranging from $2K to over $100K.

Some business credit cards come with interest-free periods. However interest rates can be very high, especially if minimum monthly repayments are not met and the card is not paid off in full.

Business credit cards can have high fees and charges, even when they aren’t in regular use.

A business credit card can be used for:

- Paying suppliers

- Buying stock or supplies

- Equipment purchases

- IT upgrades

- Vehicle maintenance

Prospa. Funding solutions to match your business needs

We’re Australia’s #1 online lender to small business.

Choice

Borrow up to $500K with 10 minute application, fast decision and funding possible in 24 hours.

Support

Confidence

Talk to a business lending specialist

Talk to a business lending specialist

Talk to a business lending specialist

Talk to a business lending specialist

Talk to a business lending specialist

Customers making it happen with a Prospa loan

Read customer stories

FAQs

Frequently asked questions

It’s important to compare business loans when you’re looking for finance for your business. But the ‘best loan’ for small business depends on the small business and what you want to use the loan for. Above you can see a snapshot of many of the business finance choices and types of loans, including equipment finance, secured business loans, unsecured business loans, line of credit products, business credit cards and more. It’s really up to you which is best for your business.

Prospa offers Small Business Loans of between $5,000 and $150,000 with funding possible in 24 hours so you don’t miss opportunities. No asset security required upfront to access Prospa funding up to $150,000. The application process is quick and easy – taking around ten minutes – with flexible lending criteria.

Business loans vary widely – including the loan terms they offer. Some business finance products come with no loan term at all (like a credit card), others are short term (like a small business loan) while others can range up to 10 years (like a traditional business loan from a bank). Many loan providers take your loan amount into consideration when they set their loan term – plus a number of other factors.

Prospa offers Small Business Loans with loan terms from 3 – 36 months, and fixed daily or weekly repayments that work with your cash flow. When you are doing a business loan comparison or applying for a business loan, you can ask the finance provide what loan terms they offer.

This is a common question, but business loan interest rates vary due to many factors. These include the type of facility (business loan, equipment loan, business overdraft, line of credit, credit card etc), the amount borrowed, what business assets the funds will be used for, whether the funds are unsecured or secured, whether it is a fixed interest rate or variable rate, and factors such as the industry the business operates in, how long the business has been running, whether the business has sufficient cash flow to support the loan, and the overall ‘health’ or creditworthiness of the business. It’s best to talk to our friendly customer service team to see how they can help you get the best business loan interest rate for your business.

Other questions?

Awards, thanks to you

It’s nice to know we’re doing something right

| Year | Award | Category |

|---|---|---|

| 2024 | The Adviser Magazine's Product of Choice: Non-Banks Survey | Winner, Best short-term loan |

| 2024 | FINNIES Fintech Australia Awards | Finalist, Excellence in Business Lending |

| 2024 | The Adviser Magazine's Product of Choice: Non-Banks Survey | Winner, Best SME loans less than $250K |

| 2024 | Great Place to Work | Recognised as one of the Top 10 Best Workplaces in Technology |

| 2024 | Work180 | Recognised by WORK180 as one of Australia’s top 101 workplaces for women |