- HY20 loan originations of $306.8 million, up 37% on the prior corresponding period (HY19: $224.5 million) and ahead of November guidance[1].

- Average gross loans of $428.9 million, up 46% on the prior corresponding period (HY19: $293.0 million) supported by ongoing expansion of Prospa’s funding facilities.

- HY20 revenue of $75.6 million up 12% on the prior year (HY19: $67.7 million) and in line with November guidance.

- HY20 earnings before interest, tax, amortisation and depreciation (EBITDA) of $4.3 million, 7% ahead of November guidance.

- HY20 loan impairment ratio[2] at 6.6%, a 28% improvement on prior half.

- Prospa has now delivered approximately $1.4 billion of loans since inception.

- Total customer numbers in Australia and New Zealand grew to 26,900 in HY20, up 45% on the prior corresponding period.

- Organisational update with Greg Moshal as Chief Executive Officer and Beau Bertoli as Chief Revenue Officer.

- Prospa is ranked first in the non-bank financial services category on independent review site TrustPilot, with over 4,800 reviews and a rating of 4.9/5 and its Net Promoter Score remains in excess of +77.

Prospa Group Limited (”Prospa” or “the Company”), Australia’s number one online lender to small business, is pleased to announce its results for the six months ended 31 December 2019 (HY20).

Total loan originations for HY20 were $306.8 million, bringing originations for the calendar year (CY19) to $583.0 million, up 34% on the prior year (CY18: $435.5 million). This exceeds guidance provided to market in November that forecast total originations of $574.5 million for CY19.

Group revenue was $75.6 million for HY20, bringing CY19 revenue to $144.4 million, up 17% on the prior year (CY18: $123.9 million) and in line with November guidance of $143.8 million. This performance was driven by strong loan originations in Australia and New Zealand.

Prospa reported HY20 EBITDA of $4.3 million and CY19 EBITDA of $4.2 million, ahead of November guidance of $4.0 million. Expenses were largely in line with November guidance.

HY20 statutory NPAT was $0.6 million (HY19: -$3 million).

Prospa’s total loan originations have now surpassed $1.4 billion, delivered to 26,900 small businesses in Australia and New Zealand, and demand continues to grow.

Prospa’s vision is to build cash flow products and services that allow small business owners to grow and run their businesses and pay for the products and services they need.

Greg Moshal said: “We continue to invest where opportunities exist to better serve our customers with new products and services, and to grow market share. We also continue to lower our cost of funding with new funding partners and leverage our scale benefits as our business evolves.”

“The proportion of originations represented by higher credit quality customers is expected to remain stable, and as a proportion of loan book will increase over time, continuing to have a positive impact on loss rates, provisioning and cost of funds.”

“The management team has adopted a tighter focus on yield management and this will remain a priority for the business as we continue to execute on growth initiatives in line with our strategy. We remain very focused on balancing risk and return as we enter the second half.”

Beau Bertoli said: “We’re focused on how we can best serve more of the $20 billion market in Australia, and the NZ$4 billion in New Zealand, providing small businesses with a number of funding options to help them grow.”

“Our originations and book continue to achieve strong growth as our business scales and deliver on our strategy. Our customer numbers are growing significantly and we look forward to finding ways to help even more small businesses in Australia and New Zealand to grow and prosper.

Improving market penetration

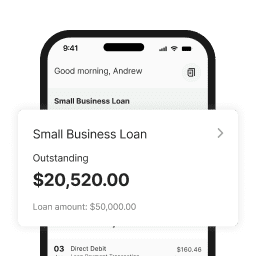

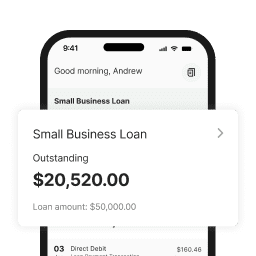

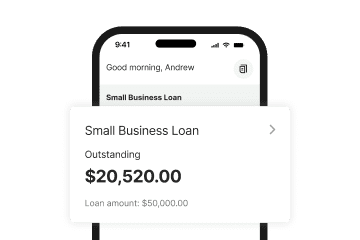

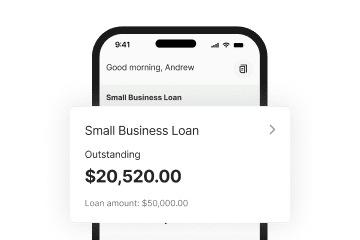

Prospa’s Small Business Loan (SBL) continues to grow strongly across Australia and New Zealand. The Prospa SBL allows small businesses to access lump sum finance of between $5,000 and $300,000 to take advantage of opportunities to invest in and grow their businesses.

Customer numbers continued to grow strongly, increasing to 26,900 in HY20, up 45% on the prior corresponding period. In the HY20 period, we saw strong customer lifetime value continue, with 2.8x loans per customer and a repeat rate of 67%.

Prospa’s lower simple annual interest rates of 9.9% to 26.5% appeal to a broader range of customer profiles. The company has continued to benefit from lower cost of funding, with the funding cost rate decreasing by 2.5% to 5.4% in HY20. As a result, Prospa’s average gross loans increased 46% on the prior corresponding period (HY20: $428.9 million).

Loan impairment expense for the period was in line with November guidance, demonstrating the improving credit quality of the portfolio. Premium risk grades represented 48% of the loan book portfolio as at December 2019 (December 2018: 34%). The proportion of the loan book that represents higher credit quality customers is expected to remain stable and will continue to have a positive impact on loss rates, provisioning and cost of funds.

The objective of improving credit quality across the loan book has always been to broaden Prospa’s customer base and access more of the $20 billion market in Australia, and the NZ$4 billion in New Zealand. Management sees many benefits of accessing higher credit quality customers including lower probability of default, improved funding costs and higher lifetime value. However, Prospa’s vision is to serve as many small business customers as possible. Management closely monitors and prices for risk to ensure that Prospa can profitably serve all segments of the market.

Lower funding costs and increased headroom

Prospa has a market leading funding platform that continues to scale. During the half, Prospa continued to actively engage with a range of capital market participants to further diversify funding sources and increase funding capacity to support the Small Business Loan and Line of Credit portfolio in Australia and New Zealand.

In Australia, an additional $52.5 million of Junior Note facilities were secured (with a right to increase to $85 million) through partnerships with top tier global and domestic investors who have a deep understanding of the Australian securitisation market, leading to a greater supply of funding and release of equity for reinvestment in future growth.

Prospa also established a New Zealand funding warehouse of NZ$45 million during the period which returned equity to the core business, allowing the Company to continue investing in growth. Over time, as the New Zealand business scales, Prospa will look to bring on board a senior funder.

At the end of the period, Prospa had $485 million in available third party facilities. A total of $33.8 million of equity capital was released and is available for redeployment in the business. Funding costs were in line with guidance.

Continued investment in product development and technology

The company has continued to focus on prioritising long term value creation and to invest in customer experience, including mobile, and as at 31 December 2019, assessing 15% of applications in real-time, double that achieved in the prior quarter.

Since its launch in the first quarter of FY20, Prospa’s mobile App is already used by 8% of the active customer base, with 25% of App users having two Prospa products. Third party payments have been enabled and 15% of Line of Credit transactions are direct payments to a supplier instead of drawdown to a bank account.

Prospa is also increasing its addressable market through the introduction of new products to market. Prospa’s Line of Credit has been well received since its full launch in October 2019. Management is now focused on ensuring Line of Credit provides a gateway to a new category of customers in line with Prospa’s objective to serve more of the small business economy. During the period, the maximum Line of Credit facility amount increased to $100,000, with an average drawn balance of $18,600 and average utilisation of 51%[3]. Originations for Line of Credit were $38.7 million for HY20.

As at 31 December 2019, the number of ProspaPay transactions in Q2 FY20 grew by 28% compared to the prior quarter, with an average transaction value of $2,400. In HY20, management are focused on securing funding and developing the Go to Market strategy for the chosen customer propositions.

Successful geographic expansion

Prospa estimates that the potential opportunity in the New Zealand market to be in excess of NZ$4 billion per annum. Progress in this market continues to exceed expectations, with Prospa originating NZ$52.8 million of loans to New Zealand small businesses to date. The company has a TrustPilot rating in New Zealand of 4.9 out of 5 and ranks first in the non-bank finance category.

The Company now has five full time employees on the ground in New Zealand, while successfully leveraging the Australian operations for administration and settlement of loans. The credit performance of the New Zealand portfolio continues to season in line with expectations.

As at 31 December 2019, Prospa had over 1,400 customers in New Zealand, with an average loan size of approximately NZ$25,000 and an average term of 12.8 months. The business has a diversified customer base across a range of industry sectors including hospitality, retail, professional services and building and trade.

Organisational update

Prospa is continuing its trajectory from a start-up Australian-centric business with one product to a fast-growth scaling business with multiple products in two geographies. To deliver on its future growth aspirations, the company has restructured executive roles and responsibilities with Greg Moshal to be the Chief Executive Officer and Beau Bertoli to take the newly created role of Chief Revenue Officer.

These changes will take effect immediately and support the company in its growth strategy and its commitment to create long-term shareholder value.

Both Greg and Beau remain significant shareholders in Prospa and will maintain their executive Board positions. Both remain in an extended voluntary escrow period until after the Company’s HY21 financial results have been released to the ASX.

Beau Bertoli said: “I’m super excited to take on the newly created role of Chief Revenue Officer and focusing on growth. The new organisational structure will allow both Greg and me to concentrate on what we do best, and in my case that is focusing on growing originations, customers and our distribution capability.”

Outlook

Prospa’s mission has always been to help small businesses to grow and prosper – an important segment of the market that has traditionally been underserved. The regulatory environment is supportive of fintech lenders to promote competition and deliver choice and better outcomes for customers, and Open Banking will deliver further opportunities. As the market continues to mature, develop and scale, the cost of funding should also become more competitive and sustainable.

Gail Pemberton, Prospa Chairman said: “Prospa continues to concentrate on long term value creation, which has resulted in impressive growth across all metrics in the period. The Board is pleased with the focus and enthusiasm in the business, and congratulates the team for putting a sharper focus on managing yield.”

Greg said: “Prospa has the benefit of being a first mover in this space, and we are not complacent. We have a huge amount of data about small businesses in Australia and we are very clear what a good small business looks like. We continue to look at ways we can add value by serving small businesses and helping them meet their goals through new products and services.”

Prospa reiterates its FY20 guidance and expects to deliver originations of between $626 million and $640 million and revenue of more than $150 million for the full financial year.

Authorised for release by the Board.

[1] On 18 November 2019, Prospa updated its guidance to the market. The Company indicated HY20 originations were expected to be $298.2 million, HY20 revenue was expected to be $75.0 million and HY20 EBITDA was expected to be $4.0 million.

[2] Loan impairment ratio equals loan impairment divided by average gross loans, annualised.

[3] As at 31 December 2019.

ENDS

For further information contact:

Company Secretary

Nicole Johnschwager

General Counsel and Company Secretary

e: [email protected]

Investor Relations

Anna Fitzgerald

Group Head of Corporate Relations

e: [email protected]

Media

Roger Newby

Domestique Consulting

e: [email protected]

+61 401 278 906

About Prospa

- Prospa provides cash flow products and services that allow small businesses to prosper

- Prospa has originated over $1.4 billion in loans to date across Australia and New Zealand

- Prospa has 26,900 small business customers

- Prospa has a Net Promoter Score in excess of +77 and is ranked #1 in the non-bank financial services provider category in Australia and New Zealand on independent review site TrustPilot

- Prospa is recognised as a 2019 Great Place to Work and was awarded AON Hewitt Employer of Choice in 2017 and 2018

- In 2018 and 2019 Prospa won Australian Fintech Lender of the Year, and achieved a clean sweep of the MFAA Excellence awards in all five States