At a glance

- Total originations have returned to pre-COVID levels faster than anticipated with 3Q21 originations of $121.0 million largely in line with the prior corresponding period (“pcp”) (3Q20: $122.2 million) and up 20% on prior quarter (2Q21: $100.7 million).

- Prospa once again experienced a strong month on month growth trend in originations over the quarter, with $30.8 million originated in January, $39.9 million in February and $50.3 million in March.

- Of the total originations for the quarter, 81% were from Prospa’s Small Business Loan and 19% were from the Company’s Line of Credit product.

- The New Zealand business continues to perform well, realising an 11% increase in originations quarter on quarter (3Q21: $19.9 million) and achieving another record month of originations in March.

- Continued focus on short and long term growth with increased investment in technology capabilities and research and development to build and trial new payments solutions in market.

- The Company’s customer centric approach is evidenced by Prospa’s Net Promoter Score of over 77[2], reinforced by a loyal customer base where long term relationships are key to growth, and customer acquisition by referral.

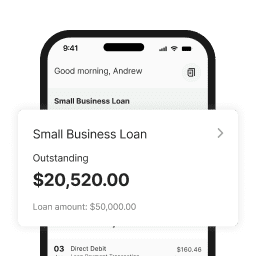

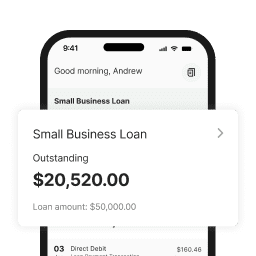

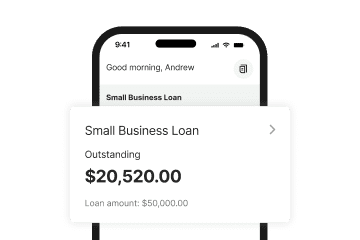

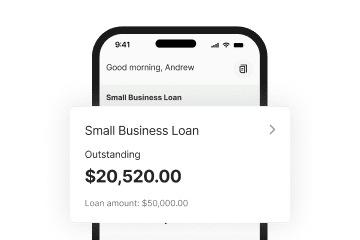

- Average Gross Loans increased to $354.0 million in the quarter with annualised yield stable for the financial year to date at 32%.

- Total revenue before transaction costs was $28.5 million, up 3% on the prior quarter (2Q21: $27.7 million) with growth in revenue signalling a post COVID turnaround point for the business.

- Prospa’s growth is underpinned by its strong balance sheet and funding platform with $449.5 million[3] in available third-party facilities ($144.4 million in available undrawn facilities[4]) and $93.2 million of cash (of which $46.0 million is unrestricted).

- Note all figures in AUD unless otherwise specified.

Prospa Group Limited (ASX: PGL) (“Prospa” or “Company” or “Group”), is pleased to provide a trading update for the quarter ended 31 March 2021 (3Q21) [1].

Greg Moshal, Chief Executive Officer, said:

“Prospa has seen better than anticipated growth in originations, driven by stronger economic confidence and investment within the SME sector. Our new loans for the quarter ended March were $121 million, which is a return to pre-COVID levels of activity for our Australian business. New Zealand has again been a highlight with originations rising 11% for the quarter, propelled by a fresh record for new loans in March.

“It is particularly encouraging to see such high levels of activity in the March quarter considering this is typically a quieter period than the busy December holiday season. This quarterly result shows good momentum for Prospa with a return to growth in revenue and average gross loans.”

3Q21 Financial Performance

The recovery in the SME sector has continued to benefit Prospa with increasing demand for the Group’s Small Business Loan and Line of Credit products. Loan originations of $121.0 million were up 20.2% on the prior quarter (2Q21: $100.7 million) and total originations for the quarter are now largely in line with origination volumes being achieved prior to the impact of COVID (3Q20: $122.2 million).

Of the total originations for the quarter, 80.8% were from Prospa’s Small Business Loan and 19.2% were from the Company’s increasingly popular and recently enhanced Line of Credit product.

The New Zealand business continues to experience strong growth with originations of A$19.9 million, up 10.6% on the prior quarter (2Q21: A$18.0 million) and up 21.3% on pcp (3Q20: A$16.4 million). Prospa continues to see record monthly originations in New Zealand and this strong growth validates the Group’s decision to expand its product offering to this market.

Total revenue before transaction costs was $28.5 million, up 2.9% on the prior quarter (2Q21: $27.7 million) signalling a turnaround point for the business following the revenue decline which resulted from COVID. Whilst revenue remains lower than the pcp (3Q20 $37.4 million), reflecting the Company’s deliberate decision in 2020 to restrain risk appetite, the business is positioned well to return to its pre-COVID revenue levels as the growth in originations continues.

As previously noted, management had taken a prudent approach to managing costs during the height of COVID resulting in lower operating expenses (3Q21: $17.8 million) versus pcp, down 13.6% (3Q20: $20.6 million).

Average Gross Loans of $354.0 million increased by 6.4% on the prior quarter (2Q21: $332.8 million) with the expectation for further growth as originations improve. This is the first time Average Gross Loans have increased since the impact of COVID and whilst they remain lower than the pcp (3Q20: $466.3 million), this quarterly growth represents another turning point for the business.

Quarterly key metrics

[1] From 29 April to 6 October 2020 originations include lending under the GGS which ended in September 2020.

[2] Total active customers as the end of each reported period.

[3] Revenue is total revenue before transaction costs.

[4] Unaudited management accounts.

Enabling small business recovery

The growth in originations back to pre-COVID levels is evidence of the strong rebound experienced by many small businesses and their increasing appetite to invest in their future. Prospa has been actively promoting its products to new and existing customers to capitalise on the pent-up demand for business investment following a long period of uncertainty in the SME economy.

Prospa continues to expand its significant database of small business insights, enabling the Company to proactively monitor for potential impacts on risk appetite and customer demand and to identify and target customer sectors and geographies where Prospa has the best opportunity to grow loan originations.

As business confidence in the economy returns, and in recognition of the need for funding flexibility in the current environment, Prospa made adjustments to its Line of Credit product during the quarter. Responding to increasing customer demand for this product, enhanced features include increasing the facility limit up to $150,000, extending the renewable term to 24 months, and providing new Pay Anyone features with scheduled and recurring payments.

During the period, Prospa was also pleased to maintain a Net Promotor Score above 77. During the height of the pandemic Prospa was able to provide relief to over 5,500 customers in the form of payment deferrals. The way in which Prospa supported its clients during this time and resultant high level of client satisfaction underpins a loyal customer base where long term relationships are key to growth, driving customer retention and acquisition by referral.

Credit risk assessment and management

The loan book is adequately covered for potential future losses and currently loan write-offs related to the impact of COVID are lower than initially expected. Static loss rates remain within the Board mandated 4 – 6% tolerance range supported by Prospa’s purpose-built credit decision engine (“CDE”). The Group continues to proactively manage credit risk on new lending using the CDE and leveraging its extensive data and industry insights.

As previously announced, the loan deferral period offered to Prospa’s customers during the height of COVID concluded in the prior quarter. Whilst the majority of these customers have now resumed repayments or paid out their facility, Prospa is working with those remaining customers on a case-by-case basis through the Company’s standard collections process. Possible losses from this group remain adequately covered within Prospa’s provisions for expected credit losses.

Loan impairment expense for the quarter was $6.7 million, representing a decrease of $2.1 million on pcp (3Q20: $8.8 million). The loan impairment expense consists of a $2.8 million increase in the provision in the period as a result of the growth in the portfolio, and $3.9 million net bad debt expense. As at 31 March 2021, the total coverage for expected credit losses as a percentage of receivables remains unchanged at 10.4% with a total provision of $38.3 million.

Solid funding platform to support business growth

Prospa’s strong balance sheet and funding platform positions the Group well to support business growth momentum. Prospa has no corporate debt and has committed funding lines from a diverse range of domestic and international senior and mezzanine funders.

As at 31 March 2021, the Group had $449.5 million in available third-party facilities including available undrawn facilities of $144.4 million with a slightly lower weighted average funding rate of 5.4% (2Q21: 5.5%), mainly due to higher utilisation of warehouse facilities.

On 17 March 2021, Prospa established a second series Trust in New Zealand to support strong origination growth within this market. During the quarter, Prospa also extended the Pioneer Trust warehouse facility and increased its limits for the Line of Credit product within multiple warehouses to ensure strong funding platforms for future growth and support increasing demand for the Line of Credit product.

By increasing efficiencies in our funding facilities, we have reduced our restricted cash balance by $16.7 million, while unrestricted cash remains at $46.0 million, bringing total cash and cash equivalents to $93.2 million at 31 March 2021. Prospa is well positioned to support increasing demand for capital from its small business customers and to leverage future growth opportunities.

Outlook and strategic opportunities

In line with the higher level of activity and improved SME confidence, Prospa has commenced increasing its investment in technology, people, sales and marketing. These costs are expected to increase from the next quarter as Prospa continues to invest in research and development and technology capabilities to build and trial new payments solutions in market and accelerate customer engagement.

Greg Moshal added:

“We are pleased with the business momentum Prospa has experienced this quarter, which has been better than anticipated. We have also seen a return to growth in the size of the loan book and total revenue. Importantly, this growth is being achieved without materially changing our risk settings, and with our robust balance sheet and funding platform, this should further strengthen our future options.

“Given the current economic outlook, we are optimistic this growth will gather pace as the year progresses due to the pent-up demand for business investment and the seasonal uplift we usually see in originations towards the end of the financial year.

“At our half year results announced in February, we outlined our long-term vision to enhance our current product set to include an integrated suite of cashflow management products, enabling Prospa to play an even greater role in the day-to-day payments and transactions within our customers’ businesses as well as supporting their growth ambitions. We will provide our shareholders with an update on this next phase of Prospa’s growth strategy in June this year.”

This announcement has been authorised for release by the Board.

Please view full ASX release with Appendix here.

For further information, please contact [email protected].

1 Note all figures in AUD unless otherwise specified.

2 Average for the period 1 January 2021 to 31 March 2021.

3 NZD converted at RBA exchange rate 0.918 as at 31 March 2021.

4 Previously referred to as “unused facilities.”